Executive Summary:

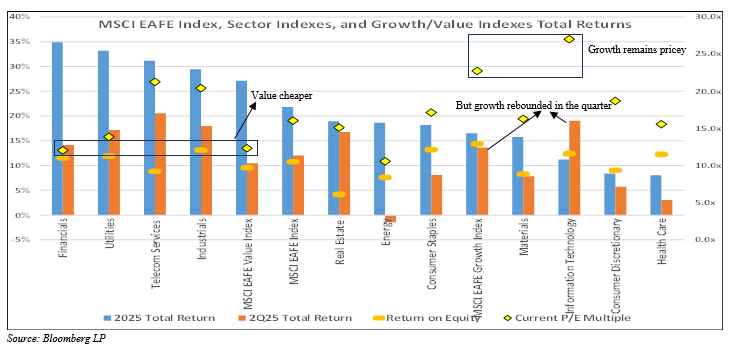

International equity markets, as represented by the MSCI EAFE Index, delivered a notable gain of 12.1% for the second quarter. This performance occurred despite heightened volatility, driven by tariff-related announcements and ongoing policy uncertainty.

The growth segment outperformed value stocks, partially reversing a prolonged three-year trend. Quality stocks continued to underperform, suggesting that investors may be seeking higher risk/reward opportunities amid policy-driven market movements.

The Financial sector led gains, benefiting from lower interest rates and steeper yield curves, which improve banking profitability.

The UK faces mounting headwinds from policy changes and increased taxation, which have spurred emigration and exerted downward pressure on the prime real estate market. Economic growth has slowed, and inflation remains stubbornly high while labor market weaknesses persist.

The European continent continues to grapple with trade-related uncertainty and subdued growth. Manufacturing activity remains weak, though employment has thus far supported domestic consumption.

Japan’s recovery is fragile, characterized by persistent – albeit low – inflation and modest GDP growth. These conditions have led to political shifts, reflecting growing domestic discontent.

Despite aggressive stimulus measures, China’s economy remains hampered by a prolonged property crisis, weak private sector demand, and deflationary trends. Credit contraction and rising debt burdens further cloud the economic outlook, even as policymakers explore supportive measures.

Overall, monetary easing and fiscal stimulus have supported global capital markets, while structural challenges, policy uncertainty, and geopolitical risks continue to temper expectations for strong economic growth.

Economic and Capital Markets Commentary

The international markets, as represented by the MSCI EAFE Index, rose by 12.1% during the second quarter, continuing trends evident during the first quarter. This strong quarterly performance belies the volatility experienced during the quarter. After President Trump’s “Liberation Day” tariff announcement, the index extended an abrupt reversal. The sharp rise in policy uncertainty weighed on prospects for economic recovery for many international economies. The index fell 14.7% from the March 18th high to its April 7th low. The drawdowns ended abruptly, and the index rose 23.9% from its low to quarter-end. Tariff uncertainty gave way, again, to greater optimism for the expansionary fiscal and monetary policy.

The overall trend during the quarter benefited growth within the broader market, though both returned over 10%. The MSCI EAFE Growth Index outperformed the MSCI EAFE Value Index by approximately 3.2% during the volatile quarter. This outperformance marginally reversed a trend that has benefited value with 13.6% in excess returns relative to growth over the last five quarters. Quality constituents also underperformed the broader MSCI EAFE Index by 1.8% during the quarter. The MSCI EAFE Quality Price Index is designed to measure the performance of “quality growth stocks” within the broader MSCI EAFE Index, focusing on high return on equity, stability of earnings growth, and low financial leverage. The more expansionary monetary policy from many central bankers provided a lower cost of capital for less attractive financial returns, buoying equity prices in more rate sensitive industries.

The valuation gap between our domestic S&P 500 Index and the MSCI EAFE Index remains wide despite the relative gains recorded during the first half of the year, with currency movements contributing significantly to the total return for US investors. For example, the discount of the MSCI Japan Index is nearly -35% currently versus a 20-year average discount of -25% (see chart below). While this valuation discount is attractive, the fundamentals for Japan remain lackluster with 2026 and 2027 earnings growth expected to lag behind that of the United States. Theoretically, some discount to valuation multiples is warranted, as both EPS growth rates and return on equity have been structurally lower for other developed markets, contributing to lower total price returns over longer horizons. This recent, wide gap may continue to provide an attractive entry for investors interested in maintaining direct exposure to international equities, diversifying currency exposure, and managing geopolitical risks, despite the significant contribution from sudden moves in currency markets earlier in the year.

The Financial sector has been the strongest performing sector for the year. Central bankers in European economies have begun to reduce their interest rates, steepening the yield curve, which can be beneficial to bank profitability, as they tend to borrow short-term while lending over longer durations. Additionally, lower interest rates and stable bank capital can contribute to increasing loan demand and bank capital returns. Furthermore, the lower interest rate environment appears to have contributed to price support for high dividend sectors, such as Utilities and Communication Services. Alternatively, the weakest sector, Health Care, has historically been considered defensive, along with Utilities and Communication Services. The Consumer Discretionary has also lagged, highlighting risks to consumption as job markets soften, tariff risks persist, and cumulative inflation takes hold.

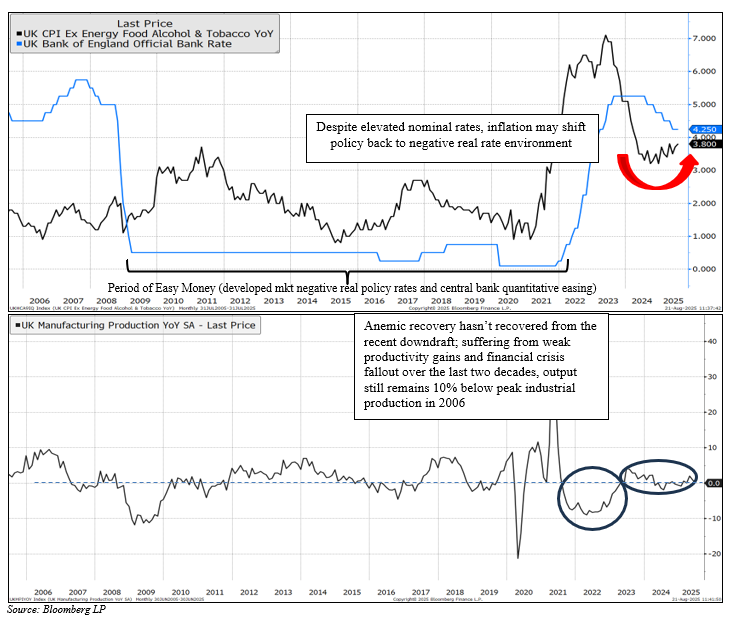

The United Kingdom has introduced a new domestic policy direction over the last few years. On the civil liberties front, they have introduced new speech laws, which, under the guise of hate speech, have resulted in mounting penalties for citizens. As the progressive Labour Party wages war on classically liberal policy, they rolled back “non-dom” tax treatment to international residents – an exclusion in the tax system dating to 1799 – as well as assessing additional taxes on private planes, capital gains, and private education. The result, according to Henley & Partners, was an estimated loss of 10,800 millionaires in 2024, a 157% increase from 2023 and more than any other country except China. The same group estimates that this number will rise in 2025 and surpass China, setting a record since Henley & Partners began tracking migration a decade ago. Much of the push for additional revenue stems from the fact that leadership has been unable to curb generous transfers, which are needed to help balance mounting fiscal deficits, as Parliament has opposed Prime Minister Keir Starmer’s proposals. This action reverses attempts to address both revenue and costs, while increasing pressure to close the fiscal gap with tax revenue. Additional taxes, including wealth levies on wealthy residents, risk further raising costs on wealth creators and risking additional capital flight. New listings in prime London markets have increased to 28% of normal levels. In comparison, buyer registrations are 5% lower, putting pressure on prime real estate in a market where prices remain 40% below their peak in the mid-2010s in real terms, according to Willow Private Finance, an independent mortgage broker in the UK. Supply appears to exceed demand in these markets, which is likely due to net emigration. Hard to know the impact these policy actions will have on the dynamism of their economy, but these policies are certainly not consistent with John Adams’ concept of a liberal marketplace.

While they wrestle with a new, less liberal policy direction, their economy shows mixed signals of resilience and fragility. The UK economy grew by 0.3% in Q2 2025, outperforming expectations of 0.1%, although slower than the 0.7% growth realized during the first quarter. Much of the growth came from the services sector and an improvement in construction activity. Unfortunately, industrial production declined by 0.3%, indicating an ongoing weakness in manufacturing activity. While inflation has fallen from its 2022 peak of 11%, the recent data have exhibited a modest re-acceleration, with Core CPI, excluding Energy, Food, Alcohol & Tobacco, rising 60bps from cycle lows to 3.8% in July. Despite the rising inflation data, the Bank of England cut its policy rates for the fifth time in a year in August to 4.0%. The central bank appears to view addressing the deteriorating labor market – with unemployment rising over 1.0% since 2022 – as the more pressing mandate [versus price stability]. In recent surveys from the Office for National Statistics, economic uncertainty remains the top challenge for trade businesses (25%), though this has declined by seven percentage points from April. For total businesses with over ten employees, the most common challenge (36% of respondents) is cost of labor. However, this has also declined modestly as the labor market has deteriorated further this year. The overall fragility is echoed by the Confederation of British Industry (CBI), which notes that Q1 2025 was likely a one-off growth surge (pre-“Liberation Day”) and that underlying conditions are complex with rising costs, a cooling labor market, and elevated policy uncertainty. Some hope remains that monetary policy can stimulate economic activity, but fiscal and social policies could offset some of the potential benefits of a credit impulse. Estimated economic growth rates over the next few years are pretty anemic at this point.

Europe is perched awkwardly between threats of export-busting tariffs and the promises of countervailing stimuli. Regionally, there have been expansionary fiscal policies (rearmament, infrastructure) and relaxation of debt breaks. At the same time, European Central Bank has been aggressive with monetary stimulus, having already reduced policy rates by over 200bps over the last twelve months. The nascent acceleration in new bank loans reflects the early signs of this anticipated credit impulse. Factory output in the Eurozone rebounded sequentially in August after suffering declines in both June and July. These earlier declines were driven by significant drops in Germany and Ireland, primarily resulting from disrupted trade and tariff uncertainty. Trade could continue to be a headwind as uncertainty persists, even as manufacturers harbor hopes of better times with fiscal and monetary stimuli. The largest economy, Germany, returned to growth in the first quarter of 2025. While the region started the year on firmer footing, the regional economy appears set to weaken during the second half of 2025. Manufacturing Purchase Managers’ Index rebounded from last year’s recessionary levels but remains in contractionary territory at 49.6 (<50 is contraction, >50 is expansion). These levels would be consistent with a real, annual GDP growth of a paltry 0.2%, which is significantly lower than the initial estimates.

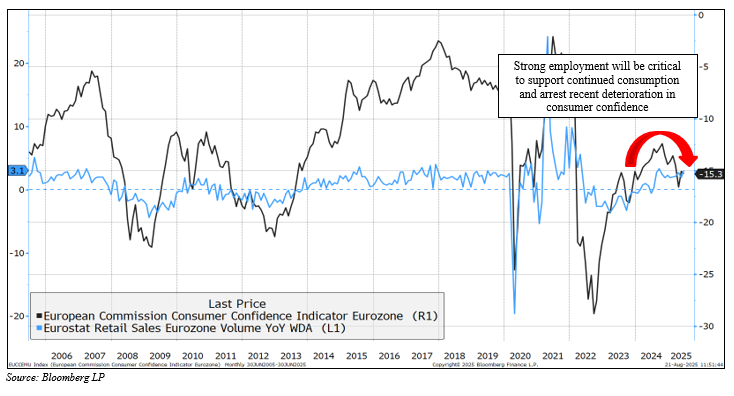

Domestic consumption will be the key engine of growth with trade uncertainty. Consumer confidence has improved from 2022 to 2023 levels, but this survey indicates some moderation in 2025. Household financial conditions and expected financial conditions contributed to the improvement, while concerns about current economic conditions remained the primary drag on consumer confidence on the continent. Fortunately, unemployment in the region fell to a multi-decade low of 5.9%, with real wages continuing to grow, supporting the recovery in retail sales, which posted a 3.1% annual increase in June. This increase was the second greatest since mid-2022. Maintaining strong employment will be key to lifting domestic consumption, but some early signs of a weakening labor market could undermine some of this economic ballast.

Japan has quietly been addressing some of its own challenges. While much of Europe appears to be trending more favorably regarding core inflation, Japan continues to see their core inflation much more elevated than over recent decades, pressuring real rates. This sets the stage for some longer-term concerns about Japan’s economy, as growth continues to slow and inflation is now stirring. The Bank of Japan, in the face of renewed inflation, has taken a more deliberate approach to managing price stability due to its historically low – and negative real – rate policy. Japan has taken initiatives over the past decade to improve the competitiveness of domestic companies, prioritizing better returns, but the central bank was slow to raise rates. Japan has returned to positive, annual real GDP growth over the last four quarters; however, concerns remain about the trajectory of this relatively weak recovery, especially after a sequential deceleration in Q2. The result of mounting pressure on the domestic consumer is evident in recent elections, where the Sanseito party, a new ultranationalist populist party, gained seats.

Trump’s economic nationalism has galvanized both Europe and China into stimulative fiscal action. In China, it has been on a scale unseen since the 2008 financial crisis. Trade uncertainty introduced a new risk to an economy still struggling under the weight of its property crisis. Weakness stemming from property markets persists after three years, and a slump in cement production reflects this drag on critical avenues for wealth creation, government revenue, and capital investment. Cement production declined by another 5% in July, reaching its lowest monthly level since 2009. Retail sales have improved from their lows in 2024 but remain structurally slower than in past decades. Retail trade decelerated again in July. This data reveals frail private demand. Other recent data from July show that China may struggle to exceed its 5% real GDP growth target during the second half. Weaker spending on infrastructure also played a key role in the slowdown. Industrial production, although weak in July, has been in a substantial uptrend since the COVID lows, following substantial industrial subsidies that have spawned new, excess capacity. In the short term, addressing overcapacity and deflation could result in weaker growth, but Beijing is likely to respond with additional supportive measures during the second half of 2025. The great unknown, as we have discussed in past reviews, remains the total amount of debt accumulated and its creditworthiness, which remains somewhat obscure. Credit outstanding for loans to households and businesses contracted for the first time since 2005, as consumers and businesses opt to reduce debt, and deflation discourages borrowing.

In 2025 and 2026, global economic growth is expected to face geopolitical risks, including ongoing armed conflicts such as those in Ukraine and the Middle East, which are likely to heighten global instability. Geoeconomic tensions – especially, between major powers such as the U.S. and China – are intensifying through sanctions, tariffs, and competition over critical resources, thereby fragmenting global trade. Cybersecurity threats and digital sovereignty disputes are escalating, with governments regulating AI and data flows, which could potentially splinter tech markets. Rising populism and protectionist policies are challenging globalization and complicating international cooperation. Emerging markets remain volatile due to political instability, and energy security concerns persist, particularly in Europe. Additionally, fiscal pressures may lead to higher taxes in some economies, which will likely weigh on potential investment and growth. Together, these risks create a complex and uncertain environment for the global economic outlook.

Mason D. King, CFA

August 21, 2025